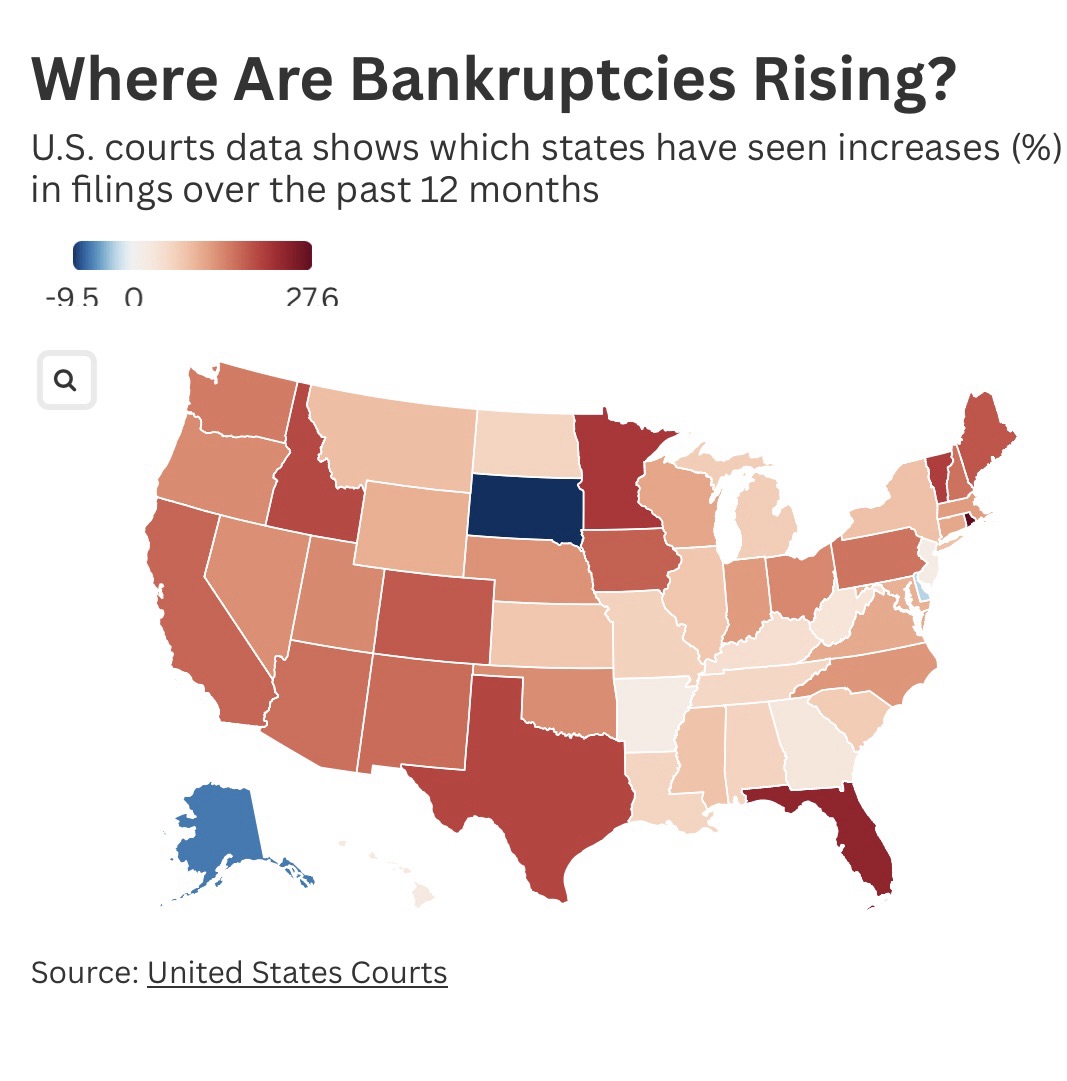

Despite upbeat official rhetoric, many Americans are struggling in deeply concerning ways. According to Experian, total consumer debt reached $17.57 trillion in Q3 2024—even though its year‑over‑year growth slowed to 2.4%, credit card and auto debt remain firmly on the rise. Mortgage balances alone stood at $12.8 trillion by March 2025, growing by nearly $200 billion in just one quarter.

Mortgages: Upside‑Down and Underwater

While mortgage debt comprises a large share of liability, the housing market shows alarming softness: home prices in major metros have declined for three consecutive months, pending sales dropped, and listings surged—suggesting demand is faltering Business Insider. Many homeowners who bought at peak prices now owe more than their homes are worth, especially if they financed with minimal down payment or took on long‐term loans.

Auto Loans: A Crisis of Negative Equity

Even more dire is the car‑loan situation. In Q2 2025, 26.6% of trade‑ins were underwater, meaning borrowers owed more than their car’s market value—an average negative equity of about $6,754. Record‑high monthly payments (often nearing $1,000) compound the burden. Auto loan delinquencies have risen across nearly all credit tiers, as younger or lower‑income buyers face worsening conditions.

Consumer Credit: Maxed-Out Spending Limits

Credit card debt surged to an inflation‑adjusted average over $10,000 per household, the first time since 2009. Rising delinquencies—spanning even high-income earners—signal widespread financial strain.

Combined, auto, credit card, mortgage, and other installment debts signal a sizable portion of the population caught in cycles of compounding interest, negative equity, and shrinking savings pools.

Contrasting Indicators: What the Headlines Hide

Economists have pointed out that even with reported 3% GDP growth in Q2 2025, much of the gain stems from volatile factors like trade stockpiling—not durable consumer strength. Consumer spending grew just 1.4% over the first half of the year, down from previous levels, and business investment is weakening amid policy unpredictability.

Consumer confidence, while inching up slightly in July to 97.2, remains volatile under the shadow of tariffs, inflation, and outbreaks of pessimism—even among wealthier households.

Economic Policy and Growing Risks

President Trump has touted a “golden age” of economic revitalization, promising lower prices and renewed strength. But critics argue that recent legislation—such as the “Big Beautiful Bill”—transfers wealth upward, cuts safety net programs like Medicaid and SNAP, and accelerates government borrowing, piling on deficits that could reach $36–40 trillion by year’s end

MoneyWeek has warned that current fiscal policies risk destabilizing the entire financial system, drawing dangerous parallels to Japan’s long‑running debt crisis. Meanwhile, analysts note the risk of stagflation, with inflation persisting even as growth stagnates—under conditions created by aggressive tariffs and credit dependency.

A Dark Age Looms for Consumers

To many ordinary Americans, the “golden age” looks more like a financial dark age. Families report skipping meals, draining savings, turning to high–interest credit options, and borrowing just to cover basics like rent and groceries. Over half of older Americans say debt has held them back—many fear they may never pay it off or retire in peace.

Despite optimistic macro‑reports, the average consumer faces mounting pressure: negative equity in autos, underwater mortgages, escalating credit card balances, and fading buying power. Unless underlying vulnerabilities—such as household over-indebtedness and unstable fiscal policy—are addressed, the American dream may slip further from reach for much of the population.

Despite the upbeat messaging from the White House, the stress endured by millions of Americans paints a far murkier picture. Without structural relief, broader safety nets, or a cooling of debt burdens, the promise of prosperity rings hollow for those living at the edge of financial ruin.